Alliance Aviation

- Patrick

- Mar 15

- 7 min read

Updated: Jul 6

Alliance Aviation Services (ASX: AQZ) is an aircraft holding company that was founded in 2002 and is the third largest owner of aircraft in Australia. Their fleet currently includes 81 narrowbody aircraft manufactured by Fokker and Embraer plus an order book of 8 more yet to be delivered.

To generate cash flow they lease their aircraft out to three types of customers:

6 aircraft dry leased to an Australian airline called AirNorth

34 aircraft wet leased to Australian airlines Qantas Airways and Virgin Australia

41 aircraft used to operate charter flights for Australian mining companies to transport employees to remote mine locations (Fly-In-Fly-Out workers)

Alliance has successfully operated since 2002 by engaging in long-term contracts where fuel prices, CPI increases and load factor risk are passed through to their customer via mechanisms in their contracts. The result has been a steady earnings stream that has held up across the GFC, a mining downturn, COVID and numerous oil price shocks. The company has historically been able to generate a 15-20% return on equity by using leverage to amplify returns to equity holders.

The 1637 Fund has a stake in Alliance Aviation (ASX: AQZ). A brief summary of the investment rationale can be found below.

Breakdown in Value

Over the last year, Alliance's share price has collapsed compared to its balance sheet. As of 31 December 2025, the company had over $1b of assets and $718m of liabilities resulting in equity of $358m. Additionally, the company has disclosed that its Embraer aircraft are carried at a $67m discount to their independently appraised value. Adding this results in a fair value of $425m compared to a current market cap of just $97m - a multiple of 0.23x.

The only reason for a business like this to trade at such a large discount to NTA is that its solvency is in question. Indeed that appears to be the case with Alliance now being a going concern:

They have fully drawn all of their debt facilities and have just $58m of cash on the balance sheet

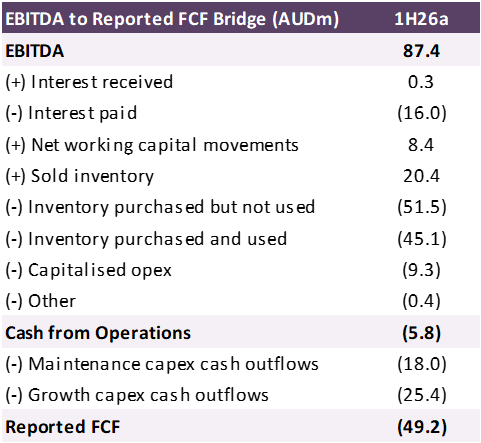

Reported FCF was negative $49.2m in the half ending 31 December 2025

They still have 8 aircraft orders scheduled for delivery in the next 12 months that will cost roughly $100m

What Went Wrong?

In late 2025 the company disclosed that they had experienced a sharp downturn in earnings as a result of their largest contract becoming onerous. The contract in question involves 30 wet leased aircraft to Qantas Airways - Australia's largest airline. To further complicate matters, Qantas is also Alliance's largest shareholder with an ownership stake of 19.7% and tried to buy the remaining 80.3% of the company in 2022 for $4.752 per share before it was blocked by the Australian competition regulator.

Importantly, Alliance has disclosed that the downturn in performance is entirely related to specific attributes of the contract with Qantas and their other contracts have been performing in line with expectations. Looking at the 1H26 result we can try and parse what went wrong:

It appears that while revenue increased by 9%, operating expenses and D&A increased by 18% and 26% respectively. This led to a sharp decline at the EBIT level of $25m, or $50m annualised. It's evident that Alliance's 'pass through' business model has broken down and that they have experienced an extraordinary or unexpected amount of costs that they have not been able to offset with increased revenue. At the result, Alliance disclosed they have commenced "a good faith commercial negotiation" with Qantas over this contract, implying they know what needs to be adjusted and where they went wrong.

At current earning levels, the company is generating just a 6% return on equity which is well below its cost of capital. Additionally the P/E multiple of 4.1x does not seem to be giving them any credit for a potential turnaround in performance.

Qantas Renegotiation

The easiest way to see a turnaround in performance would be to renegotiate key terms in the contract with Qantas. There are some reasons why this may be more likely than the market is anticipating:

Qantas is a $13b business with $1.6b of NPAT

Alliance flies 30 aircraft for them full time on wet leases, with a focus on servicing regional routes with their narrowbody aircraft so Qantas can focus on deploying their own larger aircraft on more profitable international and capital city routes

Qantas was state-owned from 1947 until 1995 and is widely considered to be the national flag carrying airline in Australia. There is a political expectation that Qantas continues to service regional routes

Qantas has no way to replace the 30 Alliance aircraft in the near term if they were to be grounded as part of liquidation proceedings

Qantas is coming off a five year period of repeated PR crises, including a data breach, fine for illegally outsourcing workers and a "ghost flights" scandal. They were recently voted as Australia's second least trusted brand ahead of only Facebook. This has led to a complete upheaval of senior management and Board members

A scenario where Qantas forces Alliance out of business despite being their largest shareholder and then cutting capacity to regional locations would put them in a difficult position politically and reputationally

With prior attempts to acquire more than 19.7% of Alliance having been blocked by the competition regulator, the only remaining choice is to renegotiate their contract to ensure Alliance's survival.

Cash Runway

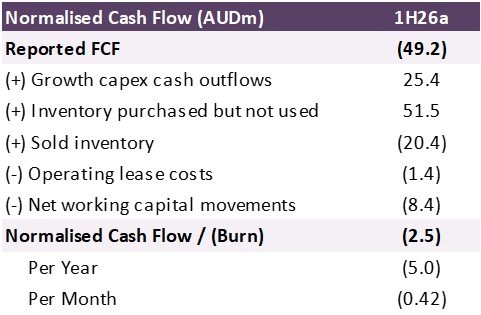

Even if Alliance is successful in renegotiating the Qantas contract, they still need a 6-12 month runway to allow them to complete negotiations and implement it. Headline reported FCF of negative $49.2m at the 1H26 result appears like little runway for a company with $58m of available liquidity. With that being said, there is a fair bit of noise in these numbers. Reconciling EBITDA to FCF can allow us to determine what is really contributing to this.

As can be seen from the above, there was a significant amount spent during the period on extraordinary (non-recurring) items including inventory purchased but not used ($51.5m) and growth capex being the delivery of 2 aircraft ($25.4m). There were also some inflows arising from extraordinary items including a positive working capital movement ($8.4m) and some inventory sold ($20.4m). If we adjust the reported FCF for these items and include the small outflows from operating leases (that is not included in FCF under IFRS 16), we see the actual rate of cash burn is more like $5m per year.

The $100m of aircraft deliveries scheduled can be either deferred, on-sold to third parties or financed with a vendor facility if Alliance wishes to deploy them as part of their working fleet. These aircraft were ordered in February 2023 and prices have increased around 20% since then due to persistent inflation. This improves the prospect that Alliance will be able to find a buyer for them. There are also other assets on the balance sheet that can be monetised, including spare hangars held as PP&E that have recently been advertised for sale.

I suspect the market is concerned that Alliance will be forced to raise capital by issuing additional shares. At the current share price, even a small amount of capital raised would lead to a significant decrease in NTA per share. Their current shareholder base makes this somewhat unlikely, with over 50% of the company held by just 4 entities - Qantas (19.7%), businessman Robert Christie (11.6%), hedge fund Viburnum (10.3%) and businessman Hugh Jones (10.0%). While Qantas is unable to increase their ownership, the others are incentivised to protect the value of their existing investments and avoid dilution unless absolutely necessary. Both Viburnum and Hugh Jones have had representatives appointed to the Board in the last six months implying they are actively engaged. Encouragingly in the last week three Directors including the Chairman have purchased shares on market. While this means a resolution to the Qantas contract is not imminent it also means they are comfortable with the long-term prospects of the business and its current liquidity runway. It also discounts the chances of a near-term capital raise.

Importantly, Alliance doesn't have any debt facilities maturing in the next twelve months and two thirds of their debt matures progressively starting in 2028 and ending in 2033. Covenants are undemanding and waivers are possible given the strong asset backing. The structure and terms of these facilities should be conducive to a business turnaround.

Asymmetric Upside

Ultimately Alliance is a highly distressed company that is trading at 0.2x NTA and a P/E of 4.1x. While priced for disaster, I have a high degree of confidence that Qantas will not allow them to go out of business. There is a significant opportunity for Alliance to do a complete review of its asset base and ensure they are earning an adequate return on all of their aircraft. If they're able to achieve this the share price should be a lot closer to the adjusted NTA of $2.64. At a current share price of $0.60 there is adequate margin of safety.

Ultimately if Alliance is able to complete the following steps in the next year or so, the share price should be multiples of its current level:

Renegotiate the contract with Qantas, restoring the earnings and cash flow generation of the business to adequate levels

Either sell or secure a funding solution for the $100m in aircraft deliveries due over the next twelve months that doesn't involve issuing equity

Lastly, we are currently 16 days into a new Gulf war between the U.S., Israel and Iran that has caused considerable disruption to oil supply chains. For now the markets seem to be pricing in a fast resolution to the war and a subsequent restoration of supply chains. While higher fuel prices will be passed through to customers, Alliance could be vulnerable to jet fuel shortages or demand destruction for flying. Australia seems to have a safe cushion of land and floating reserves to avoid fuel shortages in the near future. In the longer term they will attempt to leverage their position as a large exporter of natural gas and coal to secure fuel from Asian refineries. Alliance is somewhat protected from demand destruction as a result of operating smaller aircraft - if passenger numbers go down it's generally the larger aircraft that become less profitable to operate (think of the difference between operating a 200 seat aircraft at 50% capacity versus a 100 seat aircraft at 100% capacity). Additionally, Alliance has a strong business flying for Australian mining companies who will likely see some higher demand based on stronger commodity prices.