Predictive & Robex Merger

- Patrick

- Oct 5, 2025

- 5 min read

Updated: May 23

This morning, African gold explorers Predictive Discovery (ASX: PDI) and Robex Resources (ASX: RXR / TSX: RBX) announced they had agreed to a merger of equals to create one of West Africa's largest gold producers.

Predictive Discovery owns a 5.5 Moz gold project in Bankan, Guinea. They received environmental approvals earlier this year and are now in the final stages of the application process for an exploitation permit from Guinea's government. The expectation is that they will begin construction in 2026 and pour first gold in late 2027.

Robex Resources owns a 4.0 Moz gold project in Kiniero, Guinea. They have already commenced construction and expect first gold production in late 2025. Importantly, Robex's Kiniero project is located just 25km from Predictive's Bankan project. This creates a strong rationale for the merger, effectively creating one mega-project. Robex also owns a small mine in Mali that is coming to the end of its useful life and largely immaterial.

The transaction is being structured as a merger of equals, with Robex shareholders receiving 8.667 Predictive shares for each Robex share. Upon closing, this will result in Predictive shareholders owning 51% of the MergeCo and Robex shareholders owning 49%. MergeCo's management team will be led by current Robex Managing Director Matt Wilcox, who has extensive experience building gold mines in Africa including the soon to be completed Kiniero project. MergeCo will be Chaired by current Predictive Managing Director Andrew Pardey. All key personnel have significant ownership stakes in their respective companies and are positively aligned with shareholders.

The 1637 Fund has taken a stake in the combined entity by acquiring shares in Predictive Discovery (ASX: PDI). A brief summary of the investment rationale can be found below.

Possibility of a Counter-Bid

Predictive has three large strategic gold miners on its register that have adequate scale and rationale to make a counter-bid to the Robex proposal. Perseus Mining (ASX: PRU) owns 17.8%, the Lundin Family owns 6.5% and Zijin Mining (HK: 2899) owns 3.5%. All have long and successful track records in West African gold mining.

Importantly, the structure of the merger means Predictive (with its primary listing in Australia) does not need shareholder approval for the transaction to proceed. There is a customary fiduciary provision that allows Predictive to terminate the merger if they receive a proposal the Board considers to be superior. As such, the Fund has decided it would be prudent to own Predictive shares rather than Robex shares. After one day of trading in Australia, Predictive is trading at a slight premium to the current merger ratio.

Significant Index Fund Inflows

Predictive and Robex are not large enough on their own to be included in the major Australian & International equity gold indices. As of today, MergeCo has a pro-forma market cap of $1.7b USD and will be added to the ASX200, GDX and GDXJ indices at their next rebalancing in March. This creates forced buying equal to 5-7% of the MergeCo's total shares outstanding. This will likely provide a continued near-term re-rate if the merger proceeds that will gradually manifest over the implementation schedule.

Undemanding Valuation

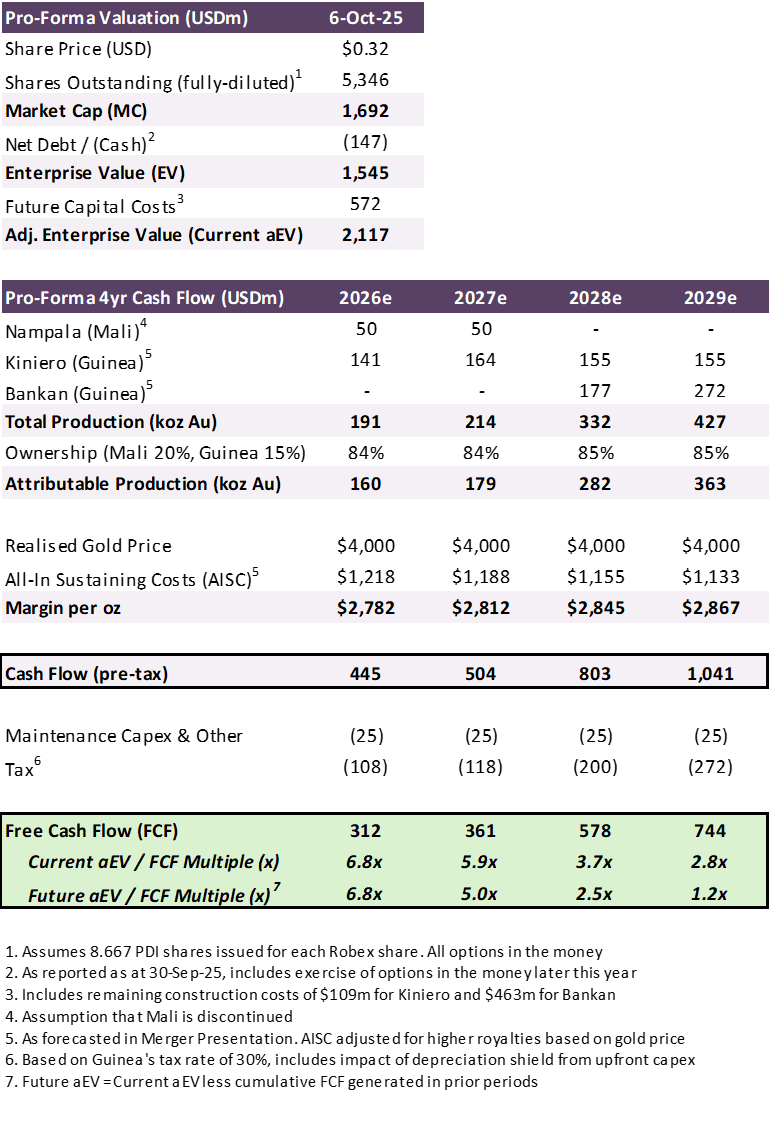

Based on the current share price of $0.32c, when Kiniero & Bankan both ramp up to full capacity over the next few years, MergeCo will be producing ~360,000 ounces of gold per annum. Assuming current gold prices remain steady over that period, that translates to $744m of annual FCF against a current Enterprise Value (EV) of $1.5b and future capital costs of $572m - a multiple of 2.8x.

Furthermore, MergeCo is expected to start generating FCF in 2026 as Kiniero starts producing an estimated 141,000 ounces which at current gold prices will generate $312m of FCF - a multiple of 6.8x the current EV & future capital costs. The FCF generated by Kiniero will be more than adequete to fund Bankan's construction, removing any risk of future dilution from an equity raise. If this future FCF is subtracted from the current EV, by the time Bankan is at full capacity in three years, the multiple will be just 1.2x FCF.

Jurisdictional Discount

It's safe to assume the market will apply a heavy jurisdictional discount to these assets given they are located in Mali and Guinea.

Mali is currently a challenging jurisdiction. It's currently led by a military dictator with the strongest opposition coming from an Al-Qaeda affiliated organization. MergeCo's asset in Nampala is coming towards the end of its life and is not considered to be cruicial to realizing the projects in Guinea. Robex recently re-negotiated the terms of their licence with the government and there's an assumption that will be adequete to continue operations until the end of 2027 at which point it can be shut down or divested for an immaterial amount. If the mine is forced to be closed sooner, that would have little impact on MergeCo's valuation given the project is coming to the end of its useful life, has lower production and higher costs.

Guinea on the other hand has a more stable outlook and is one of Africa's better jurisdictions at the moment. An unpopular dictator was replaced in a military coup in 2021. General Mamady Doumbouya has served as interim President since and has committed to transitioning Guinea back to a civilian democracy. Last month, a referendum was held that saw a new constitution approved by 89% of voters. A presidential election is expected to take place later this year that would see Doumbouya as the heavy favorite to win a five year term. Guinea has a much more favorable attitude to mining and foreign investment and is home to the world's largest iron ore mining project in Simandou, operated by Rio Tinto. There is an established mining code that has been unchanged since 2013 and the regulator has taken a sensible approach to encouraging further investment. While there is always risk owning assets in Africa, the risk-reward equation seems to be favorable in this instance. Furthermore, there is a prospect for a heavy jurisdictional discount to gradually unwind as Guinea completes its transition from a dictatorship to a democracy with political stability.

An Attractive Gold Investing Environment

Lastly, it's an attractive time to be investing in gold. Spot prices are sitting at roughly $4,000 USD and have doubled over the past two years.

The following factors have contributed to recent gains:

Heightened geopolitical tensions in Europe (Ukraine) and the Middle East (Gaza, Iran)

Increased demand from central banks in order to diversify reserves away from USD denominated assets after Russia's foreign exchange reserves were frozen in response to the war in Ukraine

Increased demand from Chinese speculators after cryptocurrency bans went into effect

Structural budget deficits across the developed world including in the United States leading to higher inflation (gold has historically acted as an inflation hedge)

Expectations of interest rate cuts across the developed world including the United States (lower interest rates reduces the opportunity cost of holding gold instead of bonds)

While the increase in gold price has been the result of a perfect storm, prices only need to remain flat over the next few years to result in significant cash flow generation at MergeCo.